The world of college financial aid is changing rapidly. This is your guide to a key component: the Student Aid Index (SAI). This essential number is the new standard in the 2024-25 FAFSA, the Free Application for Federal Student Aid. Explore how it changes the financial aid picture, its potential impact on students and families, and how to calculate yours.

What Is the Student Aid Index?

The Student Aid Index (SAI) is a new metric introduced for the 2024-25 FAFSA to evaluate a student’s eligibility for financial aid in the United States. It replaces the older Expected Family Contribution (EFC) and helps colleges determine how much aid a student can receive.

Key points about the Student Aid Index include:

Introduction: The SAI will begin with the revamped 2024-25 FAFSA, which opened in a soft launch on Dec. 31, 2023. That’s a three-month delay from the usual FAFSA open date of Oct. 1 due to extensive changes under the FAFSA Simplification Act.

Purpose: The Student Aid Index aims to provide a more accurate and equitable measure of a family’s financial ability to contribute to college expenses. The government also says the new FAFSA will help 610,000 new students from low-income backgrounds receive Federal Pell Grants. Also, nearly 1.5 million more students will receive the maximum Pell Grant award.

Calculation Factors: The SAI considers family income, assets and household size. Contributors to the FAFSA form could include the student, student’s spouse (if married), student’s parents and step-parents.

Concerns: Some financial aid experts worry that the changes, while intended to simplify the aid process, could inadvertently result in less aid for some middle-class families as college costs continue to rise. They’re also concerned about the tighter timeline to make aid determinations and distribute it.

The shift from the Expected Family Contribution (EFC) to the Student Aid Index (SAI) represents a significant change in financial aid eligibility. Both metrics assess a family’s finances, but the SAI considers more information in an attempt to provide a more meaningful number.

Here’s a more detailed look at the Student Aid Index vs. the EFC:

Needs Analysis: The fundamental formula remains the same: Cost of attendance (COA) minus Student Aid Index (SAI) and other financial assistance equals eligibility for need-based financial aid. But what goes into that basic formula is different, as you’ll see below.

Terminology: The government says the term “Student Aid Index” more accurately reflects its purpose in the financial aid process. People often misinterpreted “Expected Family Contribution” as the exact amount a family would have to pay.

Implications for Financial Aid Packages: The way the SAI influences financial aid packages differs from the EFC. With its updated methodology, the SAI alters the landscape, affecting the types and amounts of aid for which students are eligible.

Treatment of Non-Taxable Income and Retirement Contributions: SAI now considers child support as an asset rather than income, as EFC previously did. In addition, payments to tax-deferred pension and retirement savings plans will no longer be included as part of the income calculation in SAI.

Asset Evaluation: SAI will now include the net worth of a business with less than 100 full-time employees. Applicants will be asked to report the net worth of all businesses, regardless of the size of the business. In addition, the net worth of a farm will also be considered an asset, excluding the value of the family’s primary residence.

Spouse’s Financials: SAI accounts for a student’s spouse’s financial information if applicable, providing a more comprehensive view of the family’s financial capacity, whereas EFC primarily focused on parents’ and student’s financial information.

Family Members Attending College: Unlike EFC, which considered the number of family members attending college, SAI no longer adjusts for this factor.

Adjustment for Basic Living Expenses: SAI considers basic living expenses and other financial responsibilities when determining a family’s financial capacity, providing a more realistic assessment of their ability to contribute.

Focus on Equity and Accessibility: The SAI aims to be more equitable in its assessment, considering students’ diverse economic backgrounds. This change is part of a broader effort to ensure that financial aid resources are more accessible to underrepresented and low-income students.

Adjustments to Contribution Ceilings and Floors: The SAI introduces new minimum and maximum contribution expectations, including negative SAI values down to minus $1,500 to reflect when a family’s financial obligations exceed their resources.

SAI vs EFC Formulas

Dependent Students

EFC=

(Parents’ Contribution from Income and Assets ÷ Number in College) + Student’s Contribution from Income + Student’s Contribution from Assets

SAI=

Parents’ Contribution from Income and Assets + Student’s Contribution from Income + Student’s Contribution from Assets

Independent Students

EFC=

(Student’s Contribution from Income + Student’s Contribution from Assets) ÷ Number in College

SAI=

Student’s Contribution from Income + Student’s Contribution from Assets

The introduction of the Student Aid Index (SAI) brings multiple changes to determining financial aid packages for college students:

Aid Amounts: The SAI serves as a benchmark for assessing financial need. A lower SAI indicates a higher level of financial need, which generally translates into greater aid eligibility. The index helps financial aid offices differentiate between levels of student aid need.

Types of Aid: The SAI directly influences eligibility for various types of federal aid, including Pell Grants, subsidized loans and federal work-study programs. It also impacts institutional aid and some state-based aid programs, as many colleges and universities use the SAI as part of their criteria for awarding their own financial aid.

Financial Aid Packages: Colleges use the SAI with the cost of attendance to create individualized financial aid packages. These packages can include a combination of grants, scholarships, loans, and work opportunities. The goal is to bridge the gap between the cost of attendance and what the SAI suggests a family can contribute, aiming to make higher education more accessible to all students regardless of their financial background.

How the Government Calculates the Student Aid Index

The specific formula for the Student Aid Index (SAI) is complex, involving various factors and calculations. However, here is a simplified overview of how it generally works:

Total Income Assessment: The formula begins by determining the family’s total income. This includes taxable income (like wages and salaries) and non-taxable income (such as child support or tax-free interest). From this total income, the formula subtracts certain allowances and deductions. These deductions account for taxes paid, living expenses, and an “Income Protection Allowance” designed to safeguard basic family living standards.

Asset Consideration: The assets of the applicant and other FAFSA form contributors are also assessed, but not all assets count equally. For example, the formula usually excludes assets such as retirement savings and the value of the family’s primary residence. The formula applies a percentage of the remaining assets (like savings accounts, stocks, and other real estate) to the SAI. The percentage applied differs for applicant assets vs. contributors’. Contributors can include the student’s parents, step-parents, or spouse (if married).

Family Size: The formula adjusts for the size of the family, but no longer for the number of family members attending college.

Final SAI Calculation: The government determines the final SAI after these adjustments and considerations. This figure is an index, not a precise dollar amount, representing an estimate of the family’s financial capacity to contribute to college expenses.

Negative SAI Values: In some cases, the SAI can be negative. This indicates that a family’s available income and assets don’t meet basic living expenses.

It’s important to note that this is a simplified explanation of a complex formula. The actual computation involves specific percentages, thresholds, and protections that vary depending on individual circumstances. The U.S. Department of Education provides detailed methodology and tables for those who want to investigate the exact calculations. For most families, however, using online calculators or consulting with financial aid advisors will be the most practical way to estimate their SAI.

Students’ personal and financial information: Date of birth, marital status, state of legal residence, and grade level. Plus, tax filing status, adjusted gross income, total assets, and the annual child support received.

Students’ parents’ financial information: Dependent students must provide their parents’ tax filing status, adjusted gross income, total assets, and annual child support received.

Students’ spouses’ financial information, if applicable: Independent students, if married, need to include their spouse’s financials, such as tax filing status, household income, total assets, and annual child support received.

2 Common Misconceptions in the SAI Calculation

Myth: Negative SAI Means Debt: A negative SAI indicates a high level of financial need and does not mean that the family is in debt to the college or owes that amount.

Myth: SAI is a Payment Amount: The SAI is a tool for determining aid eligibility; it’s not an invoice or a statement of fees due for college.

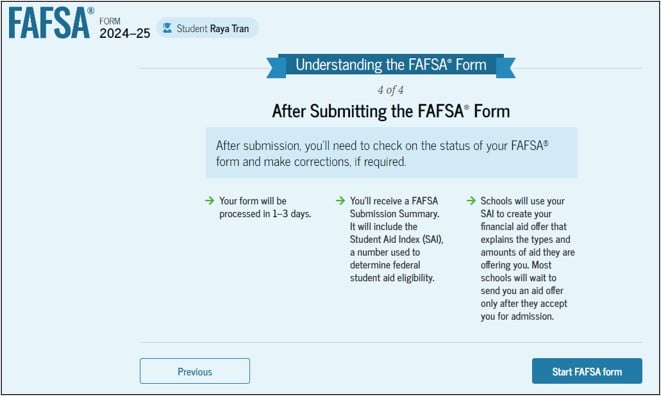

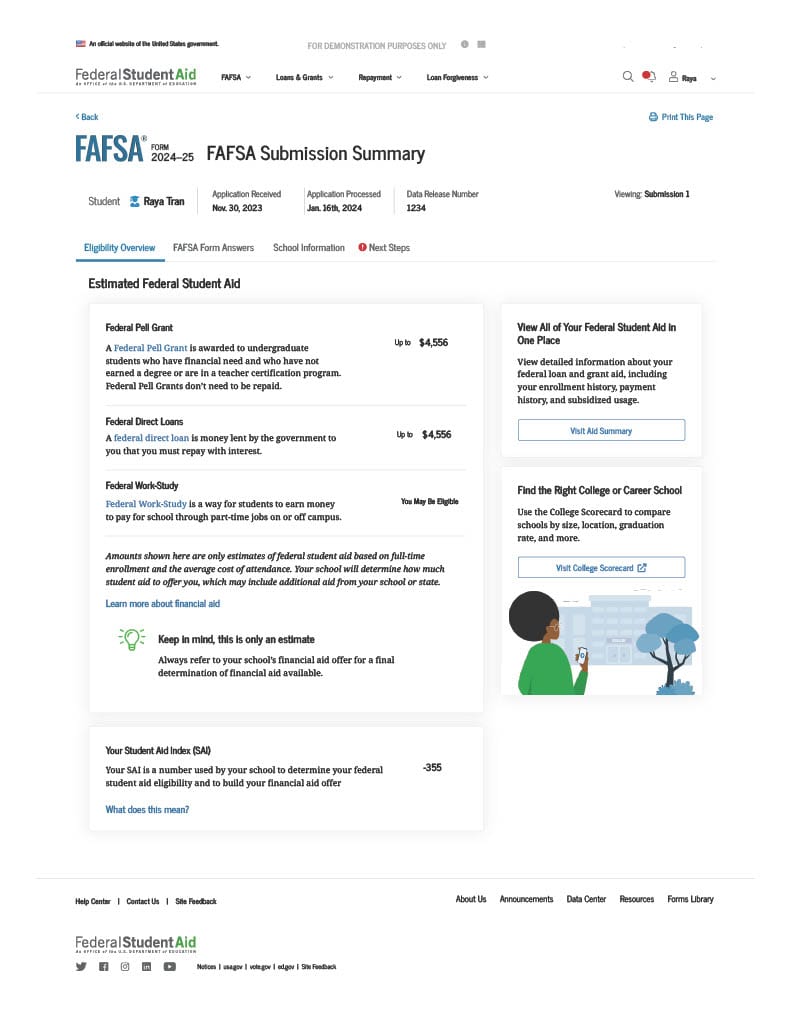

Sample screen from the U.S. Department of Education

Your FAFSA Submission Summary Will Provide Your SAI

You’ll receive a FAFSA Submission Summary, which replaces the previous Student Aid Report. This shows your estimated aid and Student Aid Index (SAI).

Here’s a sample FAFSA Submission Summary from the Department of Education. It outlines aid eligibility and the SAI and provides a link to a more detailed page, not yet available, called the “Aid Summary.”

Sample screen from the U.S. Department of Education

Improving Your Student Aid Index

Here are a few ways to reduce your Student Aid Index and potentially qualify for more financial aid:

Maximize Retirement Contributions: Increasing contributions to retirement accounts can be a strategy since these are generally not counted as assets in the SAI calculation. In addition, contributions to tax-deferred pension and retirement savings plans (excluding deductible payments to SEP/SIMPLE/KEOGH) can decrease an applicant’s or contributor’s adjusted gross income (AGI), potentially lowering the SAI.

Defer Income: You can improve your SAI by deferring income, since the year’s adjusted gross income (AGI) plays a big role in the SAI calculation. This may be more helpful for parents who receive year-end bonuses or commissions. Keep in mind that the SAI is based on your “prior, prior tax year.” So changes to 2023 income would affect SAI for the 2025-26 FAFSA.

Understand Asset Impact: Be strategic about saving and investing, as certain types of assets can affect the SAI more than others.

Start Early: Plan for college expenses early in your child’s life. The earlier you start, the more options you have for saving and investment strategies.

Seek Professional Advice: A financial advisor with experience in education funding can provide valuable advice tailored to your unique financial situation.

Top Colleges for Merit Aid With SAI Under $30,000

This crowdsourced data shows which colleges have offered the most merit aid to Road2College members so far with an SAI under $30,000. It is for the 2024-25 academic year, and much of it is repeatable in subsequent years.

College

Merit Aid Offers to Members

Under $30K SAI

# of Offers

Avg Offer

Susquehanna University

$337,000

10

$33,700

University of Arizona

$313,500

14

$23,393

University of Scranton

$261,000

10

$26,100

Seton Hall University

$243,000

12

$20,250

Quinnipiac University

$229,750

8

$28,719

Hofstra University

$228,000

8

$28,500

Wheaton College

$221,000

6

$36,900

University of Alabama

$197,362

10

$19,736

Xavier University

$193,000

8

$24,125

University of Vermont

$184,000

12

$15,333

University of Hartford

$172,000

7

$24,571

University of Dayton

$167,000

8

$20,875

Miami University-Oxford

$165,000

11

$15,000

Ithaca College

$164,000

6

$27,333

Western New England University

$162,500

5

$32,500

Hobart and William Smith Colleges

$160,500

4

$40,125

Rensselaer Polytechnic Institute

$158,000

5

$31,600

Loyola University Maryland

$155,000

5

$31,000

Merrimack College

$154,000

5

$30,800

Stonehill College

$144,000

4

$36,000

Top Colleges for Merit Aid With SAI From $30,000-$60,000

This crowdsourced data shows which colleges have offered the most merit aid to Road2College members so far with an SAI from $30,000 to $60,000 It is for the 2024-25 academic year, and much of it is repeatable in subsequent years.

College

Merit Aid Offers to Members

From $30K-60K SAI

# of Offers

Avg Offer

Susquehanna University

$692,000

17

$40,706

University of Hartford

$404,000

13

$31,077

Loyola University Chicago

$372,999

16

$23,312

University of Alabama

$352,400

20

$17,620

Fordham University

$341,335

14

$24,381

Saint Joseph's University

$324,500

12

$27,042

Seton Hall University

$300,500

15

$20,033

University of Scranton

$297,534

11

$27,049

University of Vermont

$280,000

18

$15,556

Loyola University Maryland

$270,500

8

$33,813

DePaul University

$262,000

12

$21,833

Duquesne University

$261,000

13

$20,077

Hofstra University

$257,000

8

$32,125

Drake University

$242,200

11

$26,911

Miami University-Oxford

$238,000

15

$15,867

Saint Louis University

$229,000

6

$38,167

Marquette University

$213,000

9

$23,667

Michigan State University

$211,250

14

$15,089

Widener University

$211,000

7

$30,143

Fairfield University

$210,000

10

$21,000

Top Colleges for Merit Aid With SAI Above $60,000

This crowdsourced data shows which colleges have offered the most merit aid to Road2College members so far with an SAI over $60,000. It is for the 2024-25 academic year, and much of it is repeatable in subsequent years.

College

Merit Aid Offers to Members

Above $60K SAI

# of Offers

Avg Offer

Fordham University

$628,335

29

$21,667

Fairfield University

$595,500

27

$22,056

University of Vermont

$540,500

27

$20,019

Loyola University Chicago

$525,500

22

$23,886

Quinnipiac University

$496,000

20

$24,800

Rensselaer Polytechnic Institute

$489,650

14

$34,975

University of Alabama

$486,900

24

$20,288

Wheaton College

$470,000

12

$39,167

Drexel University

$424,800

25

$17,712

Seton Hall University

$387,500

18

$21,528

Miami University-Oxford

$364,500

25

$14,580

Loyola University Maryland

$344,000

10

$34,400

University of Arizona

$337,000

16

$21,063

Gettysburg College

$335,850

8

$41,981

University of Scranton

$332,500

14

$23,750

Ithaca College

$328,500

14

$23,464

Duquesne University

$316,506

12

$26,376

Rose-Hulman Institute of Technology

$313,000

11

$28,455

Worcester Polytechnic Institute

$300,000

12

$25,000

Clark University

$296,500

11

$26,955

_______

Use R2C Insights to help find merit aid and schools that fit the criteria most important to your student. You’ll not only save precious time, but your student will avoid the heartache of applying to schools they aren’t likely to get into or can’t afford to attend.