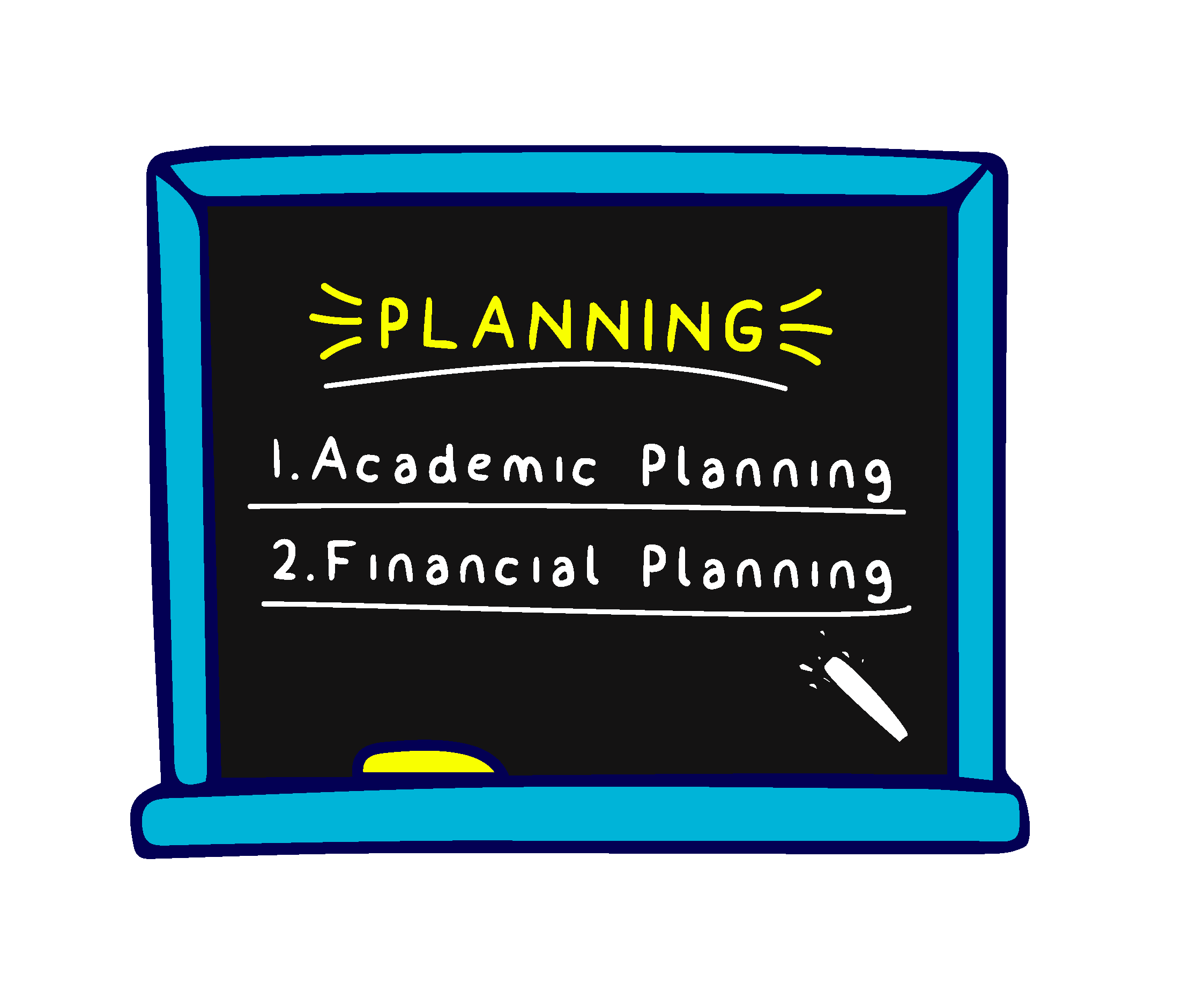

Plan

Make Financial & Academic Plans

Research

Explore Colleges & Begin Building a List

Apply

Fill Out College Applications & Financial Aid Forms

Compare

Evaluate Colleges Where Your Student Was Accepted

Decide

Determine the College That’s Right for Your Student

Pay

Understand Loan Options & How to Pay the Bill

Go

Off to College

How to Navigate College Application Deadlines in 2024

April 26, 2024 | Road2College

Choosing where to apply to college is only half the battle. There’s also the question of when. Students must decide…

Are ‘No Essay’ College Scholarships a Student’s Dream Come True?

April 26, 2024 | Monica Matthews

Editor’s Note: Monica Matthews is the author of “How to Win College Scholarships.” She helped her son win over $100,000…

Dear Roadie: My Son Told Me to Butt Out, Then Got Rejected by His Top Colleges. What Now?

April 20, 2024 | Road2College

Dear Roadie, My excellent, motivated student wouldn’t let me anywhere near the application process. He insisted he had it handled,…

Dear Roadie: Should I Drug-Test My Son to Ensure He’s Not Wasting His College Tuition?

April 12, 2024 | Road2College

Dear Roadie, My son will be attending a school that costs $80,000 per year. Am I crazy for wanting him…

How Much College Can You Really Afford? Take These 3 Simple Steps For The Answer

April 12, 2024 | Sabrina Malone

After sending four kids to college with a fifth on the way there soon, I’ve learned a thing or two…

Dear Roadie: Should I Tell My Daughter Not to Bother Applying to Unaffordable Dream Schools?

April 26, 2024 | Road2College

Dear Roadie, We just returned from visiting a few colleges and I’m feeling deflated. My daughter is a high-stat student…