One of the biggest issues that face students and parents is how to pay for college. Keeping pace with rising college costs is a huge challenge, and parents might be wondering how much they can afford to put toward college — and where they can find the money to close the funding gap.

Trying to find the answers can be tough. A recent survey of almost 400 parents in our Paying for College 101 Facebook Group, sponsored by College Ave Student Loans, found that 66.5% of parents expect federal student loans to play a role in college funding. This is a slight uptick from 65% a few months ago when a similar survey was administered in the fall of 2019.

In fact, 52% of respondents know how much they can afford to pay for college — and they know it won’t happen without some degree of debt. Here’s what we learned about how students and parents are preparing to pay for college.

How Much Will I Need to Borrow for School?

Of the respondents who report needing loans to help pay for college, 48% feel that they will need to borrow less than $10,000 per year. This is a drop from the fall of 2019 when 54% reported thinking they could borrow less than $10,000.

How much will you need to borrow?

More people are starting to realize that they might have to borrow more in order to close the college funding gap. Nearly 8% of respondents in the most recent survey believe they will need to borrow $20,000 a year — as compared to about 6% in the previous survey.

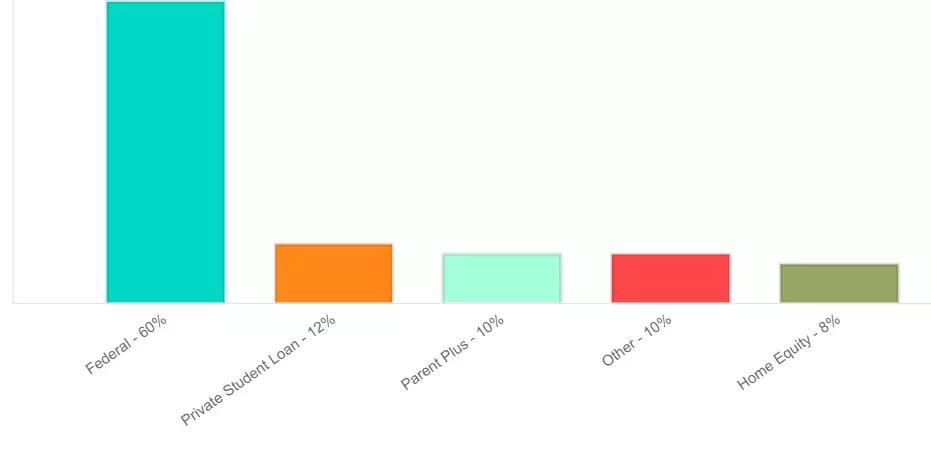

While 66.5% of respondents know they will need federal student loans to pay for school, 43.4% believe they will need . This is a rather large jump from the 32% that expected to need private student loans in the fall of 2019.

This increase in expectations for private student loans comes with a somewhat worrying trend — many don’t actually understand how the student loan process works.

In fact, 58% of respondents say they don’t understand the federal loan process and 71% say they don’t understand the private loan process . While resources like College Ave try to provide education as well as student financing, the reality is that many students and parents feel overwhelmed by the process.

Many respondents in our survey offered advice focused on starting early to understand how to move forward.

“Start researching yesterday,” wrote one respondent. Another suggested that you “Start well before high school so you can understand the factors in the process.”

However, even with this lack of knowledge, there is hope. “Don’t despair,” one respondent assures others. “There are options out there. Keep an open mind.”

By understanding federal and private loans, and how they work, it’s possible to close the college funding gap after other resources have been exhausted.

Use a 529 to Save

The survey indicates that 60% of respondents are using some type of account to save for their students’ college educations.

For those saving for college, 529s are the most important vehicle. In fact, 71% of respondents say they have a 529 to help their student save. This is a slight increase from the results of the fall 2019 survey when 68% of respondents claimed to have a 529.

What type of savings products do you have?

A 529 plan is by far the most popular choice. Part of the reason is likely the fact that money can be invested and grow tax-free when used for qualified education expenses.

The money you contribute is after-tax, but the fact that it grows in a tax-advantaged manner can be an advantage. You don’t have to worry about capital gains taxes as long as the money is used appropriately.

Many respondents recommend starting as early as possible — even while your child is a baby. The longer the money has to grow, the less likely you are to need to borrow to pay for college.

“Start saving early, even if it’s only a little a month,” suggests one parent. Later, you can increase your college contributions. But the longer the money has to earn compounding returns, the better off your student is likely to be.

Another parent suggested trying to turbo-charge saving during the high school years:

“If you haven’t been able to save a lot for college prior to high school, it’s not too late. Go big for those four years, then you know you can cash flow that same amount if necessary while the child is in college. We are saving $15,000 a year while our daughter is in high school.”

Talk to Your Child About College Costs Early and Often

In our society, it’s still somewhat awkward to talk about money. However, the earlier you talk to your child about college, the better off everyone will be.

This survey is encouraging because it indicates that more parents are seeing the need to speak to their children about how to pay for college. Last fall, 75% of parents said they had the money talk with their students. In the most recent survey, 80.5% of parents have had that talk.

Letting your child know what to expect is a huge part of planning to pay for college. You need to be on the same page. Otherwise, your child might think you’re paying for the whole cost when you might not be willing to pay as much as they think.

Be realistic about how much you can afford. Most respondents in the survey had an idea of how much they could afford for college — and that’s great. Now, though, it’s important to share that information with your students.

Do you know how much you can pay for college?

Part of the talk about how to pay for college includes a realistic discussion of where your child might be able to attend school.

“Try to make college decisions from a factual standpoint, not an emotional one,” one respondent warns. “Do not get caught up in the dream school mentality.”

While it’s nice to have your sights set on one school, it’s also important to avoid saddling your child and yourself with lots of debt, just to go to a certain school.

Using a net price calculator (NPC) can make a huge difference in understanding costs and seeing whether a school is truly affordable.

“Run the NPC for each school,” says another respondent. “This takes time as the list evolves. Share the info with your student. Discuss financial expectations and responsibilities of parent and child.”

Options for Reducing College Costs

Part of the money talk has to be about reducing college costs. Some of these options might not be palatable for the student, but it’s still important to review the options and let your child know there are choices. Some ways to reduce college costs include:

- Starting at community college

- Considering a public school instead of a private school

- Working during school

- Using work-study if you qualify

- Applying for merit scholarships

- Filling out the FAFSA to qualify for need-based aid

By looking at more options, your student might make better decisions. According to the most recent survey, 78% of respondents feel that they have a “financially balanced” college list. Making sure the list is financially balanced is an important part of providing different choices.

If your child gets scholarships and other aid to help reduce student loan borrowing for a more expensive school, that’s great. However, having a list of other choices that are more affordable can provide a way for you to shift gears if the first choice proves more expensive.

Create a list that includes low-cost schools as well as expensive dream schools.

The process of applying for aid isn’t much clearer than student loans, unfortunately. Only about 52% of respondents say they understand how to search for colleges that offer scholarships based on need and merit.

Advice from Parents on How to Pay for College

One of the biggest pieces of advice is to calculate four to five years of cost.

“It’s heartbreaking to see families scrape by the first year, and have no game plan for the next three,” writes one respondent.

In fact, many parents either plan all four years at once or at least look ahead, using a combination of year-by-year planning and holistic planning.

Understanding the total cost can change the formula and help students and parents make different choices about paying for college.

How far in advance do you budget for college?

Other parents suggest taking a hard look at the application process and making a plan to focus on schools where you might have a better chance of financial help.

“Understand the strategy of applying,” suggested one. “Is your child high stats or more holistic? What are the chances of merit aid at a particular institution? I didn’t understand the difference between colleges that were focused on pure stats with auto merit vs holistic until it was too late.”

Make sure you fill out the FAFSA each year for college, too.

First of all, the FAFSA is used to determine need-based aid from the government, as well as from many schools. Additionally, as your family’s situation changes, you might end up eligible for more aid later. Keep up with the FAFSA.

Additionally, another parent suggested that it might make sense to keep saving. “Continue saving in a 529 if you have one while they are in college and if you are able to do so. Funds continue to grow and are there for later years of college or grad school.”

It’s possible to change the beneficiary for 529 plans, so the money can also be used for other children if needed — or even for you.

In the end, the best thing you can do is save as early as possible and begin researching for scholarships and learning the process while your child is a freshman or sophomore. That way, you’re prepared when the time comes to go through the process, and you’ll be less likely to need to borrow as much money.

“Don’t wait until graduation is near to try to figure it out,” wrote one parent. “Start early.”

This article is sponsored by College Ave Student Loans. Check out their private student loan rates and see how they compare to parent PLUS loans.