As you consider how to pay for college and familiarize yourself with how student loans work, you’ll probably wonder what the interest rates are for student loans. Your student will have to pay back more than the principal alone – interest can dramatically increase the overall cost of school.

The good news is that it’s possible to know ahead of time how much student loan interest rates are and to make wise choices for financing.

Federal Student Loans

Federal loans are the easiest to understand because they all have the same interest rates and fees. When you’re looking at a federal loan, they all come from the government and have standardized policies and terms.

Interest Rates

Between July 1, 2026 and June 30, 2027, interest rates are as follows:

- Subsidized and unsubsidized Stafford loans: 6.52%

- Graduate Stafford loans: 8.07%

- Parent PLUS loans: 9.07%

These fixed rates apply for the life of the loan. Every July 1, the government updates the interest rates, but the new rates only apply to new loans taken out during the year.

Federal laws can impact interest rates, of course, so it’s important to monitor what Congress is considering regarding student interest rates and loan policies.

Student and Parent PLUS Loan Origination Fees

Federal loans have fees based on the amount borrowed. The fees are a set percentage of the award amount and are deducted proportionally from each disbursement.

As of July 1, 2020, the origination fee for new Direct Subsidized and Unsubsidized Loans is 1.057 percent. The origination fee for Parent PLUS and Graduate Direct Loans is 4.228 percent.

Subsidized vs. Unsubsidized Loans

Another important element in federal student loans is whether or not they are subsidized. If they are, your student will pay less because interest will not accrue while they are in school full-time or during the repayment grace period.

Unsubsidized loans accrue interest immediately. Your student can either make the interest payments during school or add them to the loan.

If you add the interest to the loan, the amount owed will be larger, and the subsequent interest will be more because it will be charged on the higher amount owed.

Private Student Loan Interest Rates

Private loans are an entirely different beast. Dozens of banks are willing to originate these loans, and they can have a wide variety of fees, interest rates, and terms.

You want to ensure you fully understand the terms of each loan you and your student agree to. Interest will probably start accruing immediately, similar to an unsubsidized federal loan. However, you may or may not have the option to defer those payments until graduation.

Interest rates can vary significantly, and you will encounter both fixed and variable interest rates. While variable interest rates start lower, they introduce a lot of uncertainty because you can’t know what will happen in the coming years. It’s usually best to lock in a fixed interest rate if you can.

Some private loans will require your student to have a cosigner. Your student must choose a trustworthy cosigner. It’s also important for the cosigner to understand the risk and find out if there’s a way to remove the cosigner after a certain number of on-time payments.

Finally, private student loans may not have the terms and protections of a federal loan. These include income-based repayment, forbearance and deferment options, and forgiveness opportunities.

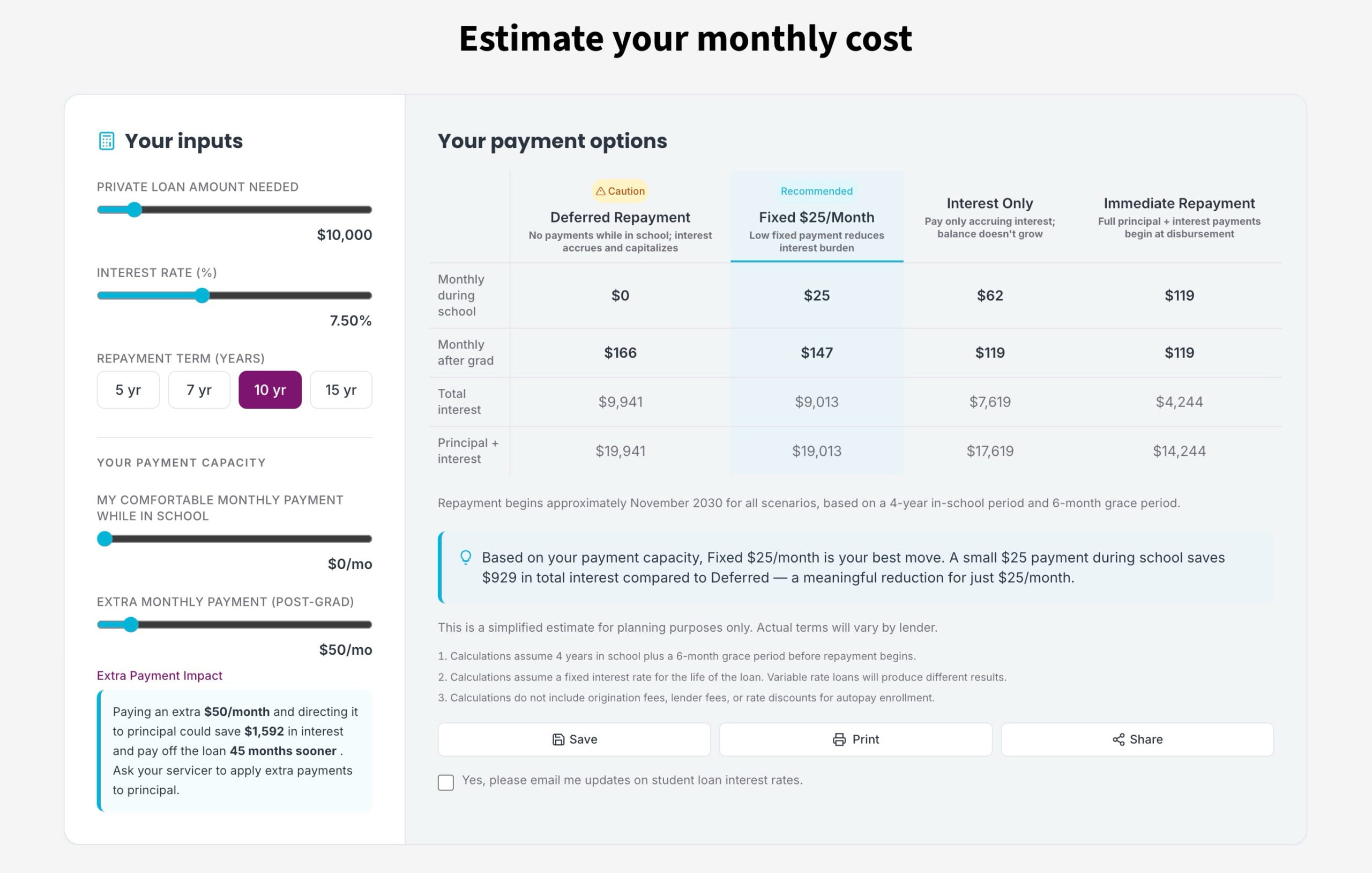

Comparing Private Student Loans

Comparing interest rates on private loans can be a major challenge, especially when you’re trying to understand the total cost. We want to make it easier for you.

Use our student loan calculator to help you understand the different interest rates lenders are offering you and the options available for each loan.

Compare Student Loan Rates From Top Lenders

| Lender | Co-Signer Release | Repayment Options | Term | Interest Rates |

|---|---|---|---|---|

| Yes | - Flat Payment (In-School) - Full (principal & interest) - Deferred - Interest-only | 5, 8, 10, 15 years | Check Rate |

| Yes | - Deferred - $25 Minimum Amount - In-School Interest Only | 5, 7, 10, 12, 15 years | Check Rate | |

| Yes | In school payment options - Pay now or later: Make interest payments - Pay a fixed $25 payment - Defer payments until after school -Undergraduate loan rates displayed. Lower interest rates shown include the auto debit discount. | 10-15 years | Check Rate | |

| Yes | - Immediate repayment - Interest-only - Fixed monthly payments in school - Fully deferred | 5, 7, 10, 15 years | Check Rate |

_______

Use R2C Insights to help find merit aid and schools that fit the criteria most important to your student. You’ll not only save precious time, but your student will avoid the heartache of applying to schools they aren’t likely to get into or can’t afford to attend.

Looking for expert help on the road to college? See our 1-1 Coaching Services.

Looking for expert help on the road to college? See our 1-1 Coaching Services.

Other Articles You Might Like:

An Expert Discusses How Student Loans Work

How Do Student Loans Work: Guide to Federal, State, and Private College Loans

Parent PLUS Student Loan Guide: How They Work, How to Get Them

JOIN ONE OF OUR FACEBOOK GROUPS & CONNECT WITH OTHER PARENTS:

HOW TO FIND MERIT SCHOLARSHIPS

SaveSave

SaveSave

SaveSave

SaveSave

SaveSave

SaveSave

SaveSave

SaveSave

SaveSaveSaveSave

SaveSave

SaveSave

SaveSave