About the author: Debbie Schwartz founded Road2College in 2014 to help families navigate the realities of paying for college. She previously worked in finance at Vanguard, Fidelity, and Accenture, and holds an MBA from MIT Sloan.

Too many families pay for college with the wrong sources in the wrong order. This guide shows the right sequence, step by step. It includes a customizable borrowing blueprint tool and a private college loan calculator to run your family’s numbers.

Inside This Article:

- The order of sources to pay for college

- Step 1: Maximize merit aid and scholarships

- Step 2: File the FAFSA (and CSS Profile, where required)

- Step 3: Draw from 529 plans and college savings

- Step 4: Pay from current income without sacrificing retirement

- Step 5: Take federal student loans

- Step 6: Compare loan options and decide who repays

- Run your numbers with our borrowing blueprint tool

- Use our private loan calculator if needed

Quick Summary:

Paying for college works best as a sequence, not a menu. Maximize free money before tapping savings, savings before income, and income before any loan. When borrowing is necessary, take federal student loans before parent or private loans, and decide who in the family will actually repay each one. Going out of order leads to over-borrowing. This guide includes a borrowing blueprint tool that runs the math for your situation. It also includes a private loan calculator.

Go straight to the borrowing blueprint tool →

The Order of Sources to Pay for College

The right order of funding sources to pay for college is: maximize merit aid, file the FAFSA, use 529 savings, pay from income, take federal student loans, then compare parent and private loans last. Going out of order leads to over-borrowing and debt that lasts longer than it should.

It’s easy to borrow before maximizing merit aid, take Parent PLUS before federal student loans, or drain savings the wrong year. The sequence is designed to prevent each of those costly mistakes.

Here’s the order that works:

- Maximize merit aid and scholarships. It’s free money that the student will get.

- File the FAFSA (and CSS Profile, where required). The FAFSA the gateway to federal, state, and institutional aid, including need-based aid. Depending on the college, you might also file the CSS Profile.

- Draw from 529 plans and college savings. It’s money you set aside for this.

- Pay from current income. It’s what you can cover from cash flow without sacrificing retirement.

- Take federal student loans. It’s the cheapest, most flexible debt available, in the student’s name.

- Compare parent and private loan options, and decide who repays. It’s your last resort, with eyes open.

A few things to know before you work through the steps:

- Your annual gap drives every decision. Net price (sticker minus aid) minus what you can pay from savings and income equals your annual gap. That’s the number you’ll close using Steps 5 and 6, if you have to use them at all. The smaller the gap, the more room you have to avoid loans entirely.

- The order matters more than the dollar amounts. Each step changes the math for the next. Skipping merit aid and going straight to Parent PLUS can cost tens of thousands over the life of the loan. A family with $80,000 in 529 savings may barely touch Steps 5 and 6. A family with no savings may rely heavily on them. The sequence applies either way.

- Run the math at each step, not just at the end. It’s tempting to wait until you’re staring at a financial aid offer to figure out what’s affordable. By then, key decisions are already made: which schools to apply to, whether merit aid was within reach. The earlier you run the numbers, the more leverage you have.

The six sections below walk through each step in order. At the end: a worked example, data on what families actually pay, and a free borrowing blueprint tool that runs your sequence for you.

Step 1: Maximize Merit Aid

Merit scholarships are free money your student earns based on academics, talent, or other achievements. Apply this money first because it directly reduces what you’ll pay before you tap savings or borrow. The right college list, with schools where your student stands out academically, can shrink your annual gap by tens of thousands.

For data on how college list composition drives net price, see our analysis of 7,040 real college offers.

Why Merit Aid is the First Place to Look

Merit aid lowers the price tag before any other source of money has to do work. A $20,000 merit award shrinks four years of college cost by $80,000. That’s $80,000 you don’t have to find in savings, pay from income, or borrow.

It’s also the source of college funding you have the most control over. FAFSA results depend on your finances. 529 balances depend on what you saved years ago. Merit aid depends on where your student applies and how their academic profile compares to the rest of the applicant pool. Build the college list with merit in mind, and the math gets easier at every later step.

Outside scholarships, awarded by community groups, employers, civic organizations, and national programs, work the same way. They’re typically smaller than institutional merit awards, but they stack on top of other aid at most schools.

Need-based aid is the other major source of free money, and it can stack with merit. Step 2 covers how to apply for it through the FAFSA. For Step 1, focus on merit because it’s the source most influenced by where your student applies, which is the decision you control before any aid form gets filed.

Average Merit Aid Awards by School Type

Merit aid varies widely by school. According to data from the Road2College Insights college comparison platform, the average merit award at private nonprofit four-year colleges is $18,492 a year. At public four-year colleges, the average is $4,871. The middle 50% of private college merit awards falls between $10,762 and $24,885. Some private colleges offer awards above $40,000.

A few patterns worth knowing:

- Private colleges discount more aggressively than public ones. Insights data shows that about 90% of students at private nonprofit colleges receive some form of merit aid, compared with about 52% at public colleges. The average net price at private nonprofit four-year colleges is about half the average sticker price.

- The most selective schools rarely offer merit aid. Schools like Harvard, Yale, and Stanford meet need but don’t compete on merit. Look one tier below the most selective schools, where institutions are competing for top applicants.

- In-state public colleges sometimes offer the deepest merit aid relative to cost. A $5,000 merit award at a $25,000 in-state public takes a bigger percentage off the price than a $20,000 award at a $75,000 private.

How to Position Your Student for Merit Aid

Merit aid follows a simple rule: Apply to schools where your student is in the top 25% of admitted applicants. Schools want to attract strong students, so they offer the most aid to applicants who raise their academic profile.

Use this to shape the college list:

- Look at each school’s middle 50% test scores and high school GPA. If your student is at or above the 75th percentile, they’re a strong merit candidate. If they’re below the 25th, merit aid is unlikely.

- Don’t only apply to reach schools. Reach schools rarely offer merit, because every student there is already strong. Mix in schools where your student is academically above average. Treating merit as automatic is a mistake; some merit awards require a separate application, an essay, or a specific deadline. Read each school’s scholarship page carefully.

- Apply early where it helps. Some schools offer larger merit awards to early action applicants or have separate scholarship deadlines that close before regular decision.

- Check the college GPA requirement to keep a renewable merit award each year. Keep in mind that college GPAs are often harder than high school GPAs.

- Apply for outside scholarships in the fall of senior year. The biggest national scholarships have early deadlines. Local and regional scholarships, often less competitive, are awarded throughout senior year. Don’t skip them because the awards seem small. Five $1,500 outside scholarships are $7,500. Over four years, that adds up.

Read more about the institutional merit aid strategy in this step-by-step guide to building a merit-optimized college list. Once you’ve built a list with merit in mind, you can model what your gap looks like at each school.

Step 2: File the FAFSA (and CSS Profile, Where Required)

The FAFSA is the single most important financial aid form your family will file. It unlocks federal grants, federal student loans, work-study, most state aid, and much institutional aid. Every family should file, regardless of income. Depending on the college, you might also file the CSS Profile. See more on both applications below.

How FAFSA Works in 2026

The FAFSA, or Free Application for Federal Student Aid, is a single application that determines eligibility for federal, state, and most institutional financial aid. You file it once a year, and it opens October 1 for the following academic year. The form pulls income data directly from your tax return, so most families can complete it in under an hour.

Filing the FAFSA opens the door to several types of aid:

- Federal grants, including the Pell Grant, the largest need-based federal grant, which doesn’t have to be repaid. Pell awards top out around $7,400 per year for the lowest-income families.

- Federal student loans, covered in Step 5. These are not need-based, but a FAFSA must be on file to qualify.

- Federal work-study, part-time employment awarded to students with financial need.

- State aid and institutional aid, both determined by most colleges and states using FAFSA data. Many institutional merit scholarships also require a FAFSA.

The FAFSA produces a Student Aid Index, or SAI, which replaced the older Expected Family Contribution. The SAI is a number colleges use to determine eligibility for need-based aid. The lower your SAI, the more aid your student qualifies for.

File the FAFSA as soon as it opens. Some state aid is awarded on a first-come, first-served basis until funds run out. The official form at studentaid.gov is always free, so avoid services that charge to file it.

How Much Need-Based Financial Aid Families Actually Receive

According to Road2College Insights data, the average need-based award at private nonprofit four-year colleges is $32,329. At public four-year colleges, the average is $13,790. Need-based awards usually come as grants that never have to be repaid, or as work-study the student earns through a part-time job.

Need-based aid is the largest source of free money for families who qualify, often exceeding merit aid in dollar amount. The two-stack system: a student who qualifies for both can receive merit and need-based aid in the same package. Eligibility is broader than many families assume. A family of four earning $100,000 may qualify for need-based aid at expensive private colleges, even if they wouldn’t qualify at lower-cost public ones.

CSS Profile Schools

About 240 colleges, mostly private, use a second financial aid form called the CSS Profile in addition to the FAFSA. The CSS Profile asks for more detail than the FAFSA, including home equity, small-business assets, and noncustodial parent income. Schools use it to award their own institutional aid.

If your student is applying to private colleges, check whether each school requires the CSS Profile. The College Board maintains a current list. The Profile costs $25 for the first school and $16 for each additional school, with fee waivers available for lower-income families.

State Grants and Scholarships

Most states run their own grant programs, and filing the FAFSA usually qualifies your student automatically. State aid varies widely. Some states award generous need-based grants to in-state students attending in-state public or private colleges. Others have smaller programs or merit-based state scholarships tied to high school GPA or test scores.

Check your state’s higher education agency for current programs and deadlines. Some state aid runs out early, which is another reason to file the FAFSA as soon as it opens.

What to Do If Your Family Doesn’t Qualify for Need-Based Student Aid

Higher-income families sometimes skip the FAFSA, assuming they won’t qualify for aid. That’s a mistake. Federal student loans (Step 5) require a FAFSA on file even though they’re not need-based, and some institutional merit aid also requires one.

If your family’s financial situation has changed since the tax year the FAFSA uses, contact each college’s financial aid office directly. Job loss, medical expenses, or other significant changes can support a professional judgment review, which lets schools recalculate aid based on your current situation rather than older tax data.

With merit and FAFSA-unlocked aid maximized, the next step is putting the money you’ve already saved to work. Step 3 covers 529 plans and college savings.

Step 3: Draw From 529 Plans and College Savings

A 529 plan is a tax-advantaged investment account designed for education expenses. Withdrawals are tax-free when used for qualified costs like tuition, fees, room and board, and books. If you’ve been saving in a 529 or other college account, this is the money to spend before tapping income or borrowing.

How Much to Withdraw From the 529 Plan Each Year

Spread 529 withdrawals across all four years rather than front-loading them. A family with $40,000 in 529 savings should plan to draw roughly $10,000 each year, not $40,000 in year one. Even spending preserves tax-free growth on the remaining balance and prevents a cash crunch in years three and four when costs often rise.

To calculate your annual draw, divide the 529 balance by four. Adjust if the balance has to cover more than one student or if you expect significant investment growth during college. Coordinate withdrawals with other tax-advantaged accounts, including Coverdell ESAs and UGMA/UTMA accounts, since they have different tax treatment and impact financial aid differently.

Use 529 funds on qualified expenses only. Tuition, mandatory fees, room and board, books, supplies, and required equipment all qualify. Health insurance, transportation, and most personal expenses don’t. Non-qualified withdrawals trigger income tax and a 10% penalty on the earnings portion.

Why Families Often Underuse Their 529 Savings

The most common mistake is holding 529 savings back to “have something left” while taking on loans to cover current costs. The math almost never works in your favor. Loan interest accrues at higher rates than 529 investment returns net of tax, and unused 529 funds aren’t free money you keep. They’re earmarked for education.

Two specific traps:

- Saving 529 dollars for graduate school. If your student doesn’t go to graduate school or chooses a program with strong funding, the 529 money can sit unused. The new SECURE 2.0 rules let you roll up to $35,000 from a 529 to a Roth IRA under certain conditions, but the rules are restrictive. Better to spend the money on undergraduate costs and avoid borrowing.

- Skipping 529 withdrawals to qualify for more aid. Parent-owned 529 assets count toward the SAI calculation, but the impact is small. The aid you’d gain by reducing the 529 balance is almost always less than the loan interest you’d pay by borrowing instead.

If your 529 balance covers most or all of college, Steps 4 through 6 may barely apply. If it covers a fraction, the remaining gap is what Steps 4, 5, and 6 are designed to close. Step 4 covers what you can pay from your current income.

Step 4: Pay Toward College From Current Income (Without Sacrificing Retirement)

Current income is what you can pay toward college from your monthly paycheck while school is in session. It’s the funding source most families underuse, often because they’ve never sat down and calculated what they can afford. Done right, paying from income reduces borrowing without putting retirement at risk.

How Much You Can Safely Pay Toward College From Cash Flow

A useful starting point is 10% of gross household income. A family earning $150,000 a year can typically dedicate around $15,000 annually to college costs without major lifestyle changes. A family earning $80,000 might manage $6,000 to $8,000.

This is a starting point, not a rule. The right number depends on other financial obligations like mortgage and existing debt, how much you’re already saving for retirement (if you’re behind, the percentage going to college should be smaller), how many years you have left to retirement, and whether you’re paying for one student or expect to pay for more.

Run the numbers for your family before you commit to a school. If the gap between net price and what you can pay from income plus 529 savings is too large, that’s information you need before May 1, not after.

Road2College’s borrowing blueprint tool, detailed below, models your income, savings, and borrowing across all four years so you can see the full picture before committing.

Tuition Payment Plans

Most colleges offer tuition payment plans that break each semester’s bill into monthly installments, typically four to ten payments per semester, usually interest-free with a small enrollment fee of $50 to $100.

Payment plans don’t change what you owe. They change when you pay it. They’re a cash flow tool for families paying from income who’d rather spread the bill across the semester than write one large check. Sign up through the college’s bursar or student accounts office before each semester begins.

The Retirement Test Every Parent Should Run Before Paying for College

Before paying any amount from current income, run a simple test: Will this payment require you to reduce or stop retirement contributions?

If the answer is yes, the amount is too high. Retirement savings have decades to compound. College costs are paid in four years. A parent who stops contributing to a 401(k) for four years to pay for college can lose hundreds of thousands of dollars in retirement that won’t ever be recovered.

“Unless you have a very robust retirement account, think long and hard before using your retirement to pay for college,” says Luanne Lee, a Certified College Planning Specialist with Your College Planning Coach. “You can borrow for college. You can’t borrow for retirement.”

The same test applies to borrowing in Step 6. If a Parent PLUS or private parent loan would require pausing retirement contributions to repay it, the loan is too large. Either reduce what you’re borrowing or choose a less expensive school.

This test is also where many families discover they need a different plan. If income, savings, and retirement-protected borrowing don’t close the gap, the answer isn’t to push harder. It’s to look at less expensive schools, appeal aid offers, or have an honest conversation with your student about cost.

With merit aid, FAFSA-unlocked aid, savings, and current income accounted for, you have a clear picture of your remaining gap. The next two steps close that gap with the right kind of debt, in the right order. Step 5 covers federal student loans.

Step 5: Take Federal Direct Student Loans

Federal student loans are loans the U.S. Department of Education makes to the student, with low fixed interest rates, flexible repayment options, and protections that no private lender matches. If borrowing is necessary to close your gap, federal student loans should always come before any private or parent loans.

Federal Loan Limits and Current Rates

Federal student loans have annual and lifetime borrowing limits set by Congress. For dependent undergraduates, the limits are:

- $5,500 in the first year (up to $3,500 of which can be subsidized)

- $6,500 in the second year (up to $4,500 subsidized)

- $7,500 in each of the third and fourth years (up to $5,500 subsidized)

- $31,000 lifetime limit

Independent undergraduates and dependent students whose parents are denied Parent PLUS can borrow more.

The interest rate on federal undergraduate loans for the 2026–27 school year is 6.52%, with a 1.057% origination fee. Rates are set each year by Congress and apply to all federal loans disbursed during that academic year. Once a loan is taken, the rate is fixed for the life of the loan.

These limits are intentionally lower than the cost of attendance at most colleges. The federal government caps student borrowing because it considers anything above these amounts too risky for an undergraduate to repay. If your family needs to borrow more than the federal limits, that’s a signal to revisit Step 4’s retirement test before turning to Step 6.

Subsidized vs. Unsubsidized Direct Student Loans

Federal undergraduate loans come in two types, and both should be taken in this order:

- Direct Subsidized Loans go to undergraduates with demonstrated financial need. The federal government pays the interest while the student is in school at least half-time and during the six-month grace period after graduation. This is the cheaper of the two federal loan options.

- Direct Unsubsidized Loans are available to all undergraduates regardless of need. Interest accrues from the date of disbursement, including while the student is in school. Unsubsidized interest can be paid in school to keep the balance from growing, or capitalized at repayment, which adds the accrued interest to the principal.

Take subsidized loans before unsubsidized loans when both are offered. The subsidized interest savings during four years of school, plus the grace period, can total $2,000 or more per loan.

Why Federal Direct Student Loans Come Before Parent or Private Loans

Federal student loans have features no private or parent loan offers, and skipping them costs families money over the life of the loan:

- Income-driven repayment plans cap the monthly payment at a percentage of the borrower’s discretionary income. New borrowers starting in 2026 will use the federal Repayment Assistance Plan; existing IBR borrowers retain access to that program.

- Loan forgiveness programs, including Public Service Loan Forgiveness for borrowers working full-time at qualifying public-service employers, can wipe out the remaining balance after 120 qualifying monthly payments (about 10 years).

- Deferment and forbearance options pause payments without default if the borrower loses a job or faces hardship.

- Death and disability discharge cancels the loan if the borrower dies or becomes permanently disabled.

The loan is in the student’s name, not the parent’s. The student carries it onto their credit, which is appropriate for college costs they’ll repay from post-college income. Federal loans are also the only borrowing tool with rates set by Congress rather than the borrower’s credit profile, so a student with no credit history pays the same rate as anyone else.

After federal loans are maxed, the remaining gap, if any, is what Step 6 addresses, including who in the family will actually repay each loan.

Step 6: Compare College Loan Options and Decide Who Repays

If federal student loans don’t close your gap, the remaining options are Parent PLUS loans, private parent loans, and private student loans with a parent cosigner. None has the protections of federal student loans. The right choice depends on credit, who repays, current rates, and how much room you have left in your budget after Step 4’s retirement test.

Parent PLUS Loans (and the New 2026 Caps)

Parent PLUS is a federal loan in the parent’s name, available to parents of dependent undergraduates who pass a basic credit check. There’s no income or asset test beyond that check. The current interest rate for the 2026–27 school year is 9.07%, with a 4.228% origination fee.

A new federal law, the OBBB Act, took effect July 1, 2026, and now caps Parent PLUS at $20,000 per student per year and $65,000 lifetime per student. Loans disbursed before July 1, 2026, may qualify for a transition period under the older limits. Check with each school’s financial aid office to confirm.

Keep in mind the interest rate is relatively high, the origination fee is significant, and the loan is fully in the parent’s name. Parent PLUS is on the parent’s credit, on the parent’s balance sheet, and repaid from the parent’s income.

Private Parent Loans

Private parent loans are loans in the parent’s name from banks, credit unions, or online lenders. Rates are based on the parent’s credit and current market conditions. For parents with strong credit, private parent loans often beat Parent PLUS on rate and origination fee.

Compare the all-in cost, not just the interest rate. Look at fixed vs. variable rate, repayment term, in-school payment requirements, deferment options, and what happens if the borrower dies or becomes disabled. Federal Parent PLUS is discharged on the parent’s death; most private parent loans are not.

Road2College’s Loan Comparison tool compares private lenders side by side and provides a calculator to see your potential payments.

Private Student Loans (With Cosigner)

Private student loans are in the student’s name, almost always with a parent cosigner because most undergraduates don’t have the credit or income to qualify alone. The cosigner is fully responsible for the loan if the student doesn’t pay, and the loan appears on the cosigner’s credit.

Private student loans typically cost less than Parent PLUS for borrowers with strong credit, sometimes by several percentage points. Some lenders offer cosigner release after a track record of on-time payments, which transfers the loan fully to the student over time. Cosigner release is not automatic, and approval rates vary widely. Read the release terms before signing.

Decide Who Will Actually Repay Each College Loan

Whose name is on the loan and who actually repays it can be different things, and assumptions made now show up as conflict during repayment.

A few common patterns:

- Parent takes Parent PLUS expecting the student to repay it after graduation. The loan is the parent’s legally; the student has no obligation to repay even if there’s a verbal agreement.

- Student takes federal loans the parents plan to cover. The loan is the student’s; parents can pay on the student’s behalf without legal complications.

- Family splits responsibility for a private loan with a cosigner. The cosigner is fully liable. If the student misses payments, the cosigner’s credit takes the hit.

“Have this conversation before you sign anything, not after graduation,” Lee says. “I’ve seen too many families assume their student would help repay a parent loan, only to find themselves scrambling when the bills started coming.”

Talk through who repays each loan before signing anything. The Borrowing Blueprint Report walks families through this conversation, including a slider that splits repayment between parent and student so each side can see the affordability impact.

Run the College Loan Affordability Test

Before signing any loan, run an affordability test on the person who’ll actually repay it.

For the student: total monthly student loan payments should be under 10% of the expected starting salary. A nurse expecting to earn $70,000 can manage about $580 a month. A teacher expecting $48,000 can manage about $400. Above 15% of starting salary is high risk territory, where loan payments crowd out rent, food, and savings.

For the parent: total monthly loan payments should not require pausing retirement contributions, delaying retirement, or drawing down emergency savings. If they would, the loan would be too large. The answer is to reduce borrowing, look at less expensive schools, or have a frank conversation about the school choice.

Both the affordability test and the repayment-split conversation are built into the borrowing blueprint tool, which models federal, parent, and private loans across all four years and shows the monthly burden on each side. The private loan calculator handles single-loan scenarios.

With Step 6 worked through, you have a complete picture of how your family will pay for college. The next sections show what this looks like for a real family, what Road2College data tells us about how families actually pay, and what to do if your gap is still too big.

A Worked Example: Paying for a $75,000-a-Year College

Here’s how the sequence works for one family. Let’s say the Patel family earns $145,000 a year and has $40,000 in 529 savings. Their daughter Anya was admitted to a private college with a $75,000 sticker price.

- Step 1: Maximize Merit Aid: Anya’s GPA and test scores put her in the top 25% of admitted students at this college, which led to a $25,000 annual merit award. That brought the price down to $50,000 a year.

- Step 2: Submit the FAFSA and CSS Profile: The Patels filed the FAFSA and the CSS Profile. Their income put them above the threshold for federal Pell Grants, but the college offered $8,000 in need-based institutional aid. The price after aid is now $42,000 a year, which is the family’s net price.

- Step 3: Draw from 529 Savings: The Patels divided their $40,000 in 529 savings across four years, drawing $10,000 each year. After this step, the gap is $32,000 per year.

- Step 4: Pay From Current Income: The Patels ran the retirement test and determined they could pay $14,000 a year from current income without reducing their 401(k) contributions. After this step, the gap is $18,000 per year.

- Step 5: Take Federal Student Loans: Anya took the maximum federal Direct Loan in each year: $5,500 freshman year, $6,500 sophomore year, and $7,500 in each of her junior and senior years, for $27,000 in federal loans total. In her freshman year, federal loans cover $5,500 of the $18,000 gap. The remaining freshman-year gap is $12,500.

- Step 6: Compare Loan Options and Decide Who Repays: The Patels compared Parent PLUS, private parent loans, and private student loans through R2C’s loan offers tool. They have strong credit, so a private parent loan offered a 7.5% rate compared to Parent PLUS at 8.94%. They chose the private parent loan for $12,500 in the freshman year and committed to repaying it themselves rather than passing it to Anya.

- The Result: Across four years, the Patels will pay $56,000 from 529 savings and current income, Anya will borrow $27,000 in federal student loans (her loans, repaid from her starting salary), and the parents will borrow about $50,000 in private parent loans (their loans, repaid from their income).Anya graduates owing $27,000 in federal loans. At a starting salary of $60,000, her monthly payment of about $295 is under the 10% affordability threshold. The parents’ $50,000 in private loans will cost about $580 a month over 10 years, which their income supports without affecting retirement contributions.The Patels paid for a $75,000 college without going over the federal student loan limits for Anya, without taking Parent PLUS, and without sacrificing their retirement savings. The sequence made the math work.

What Data Shows About How Families Really Pay for College

Most articles about paying for college rely on national averages from federal data sources. Road2College has something different: real financial aid offers shared by thousands of families through the Compare College Offers tool. The data shows what families at specific schools actually receive in aid and what they’re left to cover.

Average Aid Packages at Private vs. Public Colleges

The biggest pattern in R2C’s offer data is the gap between what private and public colleges discount from the sticker price.

At private nonprofit four-year colleges, the average merit award is $18,492 a year, and the average need-based award is $32,329. About 90% of students at private nonprofit colleges receive some form of merit aid. Many private colleges discount their sticker price by half or more for students they want to enroll.

At public four-year colleges, the average merit award is $4,871, and the average need-based award is $13,790. About 52% of students at public colleges receive merit aid. Public colleges typically have lower sticker prices to start, so the smaller discount still produces a competitive net price for in-state students.

The takeaway: a higher sticker price doesn’t always mean a higher net price. A $70,000 private with strong merit aid can cost the same family less than a $30,000 out-of-state public with no aid. The only way to know is to compare actual offers, not list prices.

What Families Actually Borrow to Pay for College

Federal student loan limits cap dependent undergraduate borrowing at $31,000 over four years, and many students borrow less. Parent borrowing has historically had no federal cap, which is why Parent PLUS balances often grow much larger than student loan balances.

The new 2026 Parent PLUS cap of $20,000 a year and $65,000 lifetime per student will change this for families who borrow heavily, forcing them either to choose less expensive schools or to use private parent loans for amounts above the federal cap. Either way, the era of unlimited Parent PLUS borrowing is ending.

Road2College’s Compare College Offers and Road2College Insights tools show what families at specific schools are paying after aid, including average net price by income bracket. That data is more useful for planning than national averages because it’s tied to the actual schools on your student’s list.

What to Do If the College Funding Gap Is Still Too Big

If you’ve worked through Steps 1 through 6 and the math still doesn’t work, you have options before resorting to loans your family can’t afford. The honest answer is sometimes that the school on the offer letter isn’t the right financial fit. The other answers involve appealing, choosing differently, or lowering the cost from a different angle.

How to Appeal Your Financial Aid Offer

Most colleges accept appeals if your family’s financial situation has changed since you filed the FAFSA, or if a competing school offered a stronger package. Contact the financial aid office directly, in writing, and document the circumstances.

Strong reasons to appeal include job loss, medical expenses, divorce, the death of a parent, or other significant changes since the tax year your FAFSA used. A competing offer from a peer school is also worth raising. Schools want to enroll students they admit, and they sometimes match or close the gap when the alternative is losing the student to a competitor.

Be specific. Include documentation. Ask for a meeting if the school offers one. Appeals are more often successful than families assume, but only when the request is grounded in real circumstances and presented clearly.

Choosing a More Affordable College

If appeals don’t close the gap and the math still doesn’t work, the most direct fix is choosing a less expensive school. Compare College Offers and Road2College Insights help families see net price across the schools on their student’s list, including in-state public options that often cost a fraction of a private college after aid.

This conversation is hard. Students have often emotionally committed to a specific school by May 1. But four years of unaffordable debt costs more than the disappointment of choosing a different college. Many families who make this trade later report it was the right call.

Other Ways to Lower College Costs

A few options reduce the total college bill without changing the school:

- Community college for the first two years. Completing general education credits at a community college, then transferring to a four-year school, can cut total cost by half or more. Confirm credit transfer policies in advance.

- AP and dual enrollment credits earned in high school can shave a semester or more off college, reducing total tuition.

- Federal work-study and on-campus jobs cover personal expenses and reduce what families have to send each month.

- Employer tuition assistance, available through some parent employers, can cover several thousand dollars a year of an employee’s child’s education. Check with HR before assuming this isn’t available.

- Income share agreements, where a student promises a percentage of post-graduation income in exchange for funding, exist at a small number of schools. Read the terms carefully. The total repaid can exceed traditional loan costs depending on the student’s career path.

If the gap still doesn’t close after exhausting these options, that’s important information. Step 4’s retirement test still applies. Borrowing more than the family can repay without sacrificing retirement isn’t a fix; it’s a delayed problem.

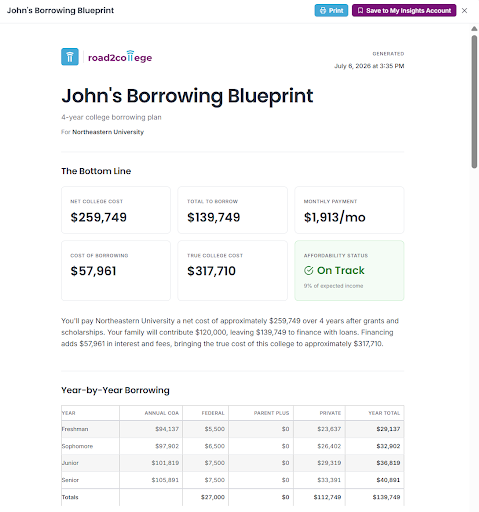

Run Your College Funding With Our Borrowing Blueprint Tool

Fill out the short form below to get your free, personalized Borrowing Blueprint. You can adjust any input afterward to see how the numbers change for your family. You can get as specific as you want on potential funding sources, including need-based aid, merit scholarships, government loans, family funds, private loans, and more. You can adjust and readjust and see the bottom line results. You can also save or print out a final report as your personal college funding blueprint.

A completed Borrowing Blueprint Report shows what your family will pay for college, what you’ll borrow, and how repayment plays out. The example below breaks down the bottom-line numbers, year-by-year borrowing across federal, Parent PLUS, and private loans, the true four-year cost after interest and fees, the 10-year amortization schedule, and the monthly payment split between student and parent. It also flags affordability risk and surfaces the assumptions behind the math, including interest rates and starting salary.

Example of a Finalized Borrowing Blueprint Report

Use Our Private Loan Calculator If Needed

Use the calculator below to estimate the monthly cost of a private student loan. Adjust the loan amount, interest rate, and repayment term to compare scenarios. For your full four-year borrowing picture, build a blueprint above.

Frequently Asked Questions About Paying for College

How Do Most Families Pay for College?

Most families combine several sources: scholarships and grants, 529 savings, current income, and student or parent loans. The mix varies by family income and school cost. The right approach is to maximize free money first, use savings and income next, and treat loans as the last resort.

Do Parents Making $120,000 Qualify for FAFSA?

Yes. Every family qualifies to file the FAFSA, regardless of income. Filing unlocks federal student loans, work-study, and most institutional aid. At expensive private colleges, families earning $120,000 may also qualify for need-based aid, since eligibility depends on the cost of the school, not just income.

How Much Should Parents Pay for College?

A useful starting point is 10% of gross household income paid annually from current cash flow, adjusted for retirement progress, other debts, and how many kids will attend college. Borrowing should never require pausing retirement contributions. If it would, the loan or the school is too expensive.

What’s the Best Way to Pay for College Without Loans?

Build a college list around schools where your student qualifies for significant merit aid, file the FAFSA to capture grant aid, use 529 savings, and pay the rest from current income. In-state public colleges or schools that meet 100% of demonstrated need also reduce the need to borrow.

How Much Is the Monthly Payment on a $30,000 Student Loan?

A $30,000 federal student loan at 6.53% over a standard 10-year repayment costs about $341 a month, or roughly $40,900 total. Private loan payments depend on the rate and term, which vary by lender and credit. Use the private loan calculator to estimate specific scenarios.

What If My Child Gets Into a School We Can’t Afford?

You have options before borrowing more than you can repay. Appeal the financial aid offer if your finances changed or a peer school offered more. Compare net prices across the schools your student was admitted to. If neither closes the gap, the school may not be the right fit.

A Note on Our Data

Merit aid, need-based aid, and net price figures cited in this article come from Road2College Insights data, covering nonprofit private four-year colleges and public four-year colleges. For-profit institutions and two-year colleges are excluded. Averages reflect schools that award the relevant aid type. Specific figures may vary year to year as schools update their reporting through the Common Data Set, IPEDS, and other sources Insights aggregates.

JOIN ONE OF OUR FACEBOOK GROUPS & CONNECT WITH OTHER PARENTS: